Fixed-Rate Mortgages: Your Guide to Stable Home Financing

When it comes to buying a home, one of the most important decisions you’ll make is choosing the right mortgage. A fixed-rate mortgage is a popular option for its predictability and stability. In this guide, we’ll break down everything you need to know about fixed-rate mortgages, including how they work, their pros and cons, and how to get one.

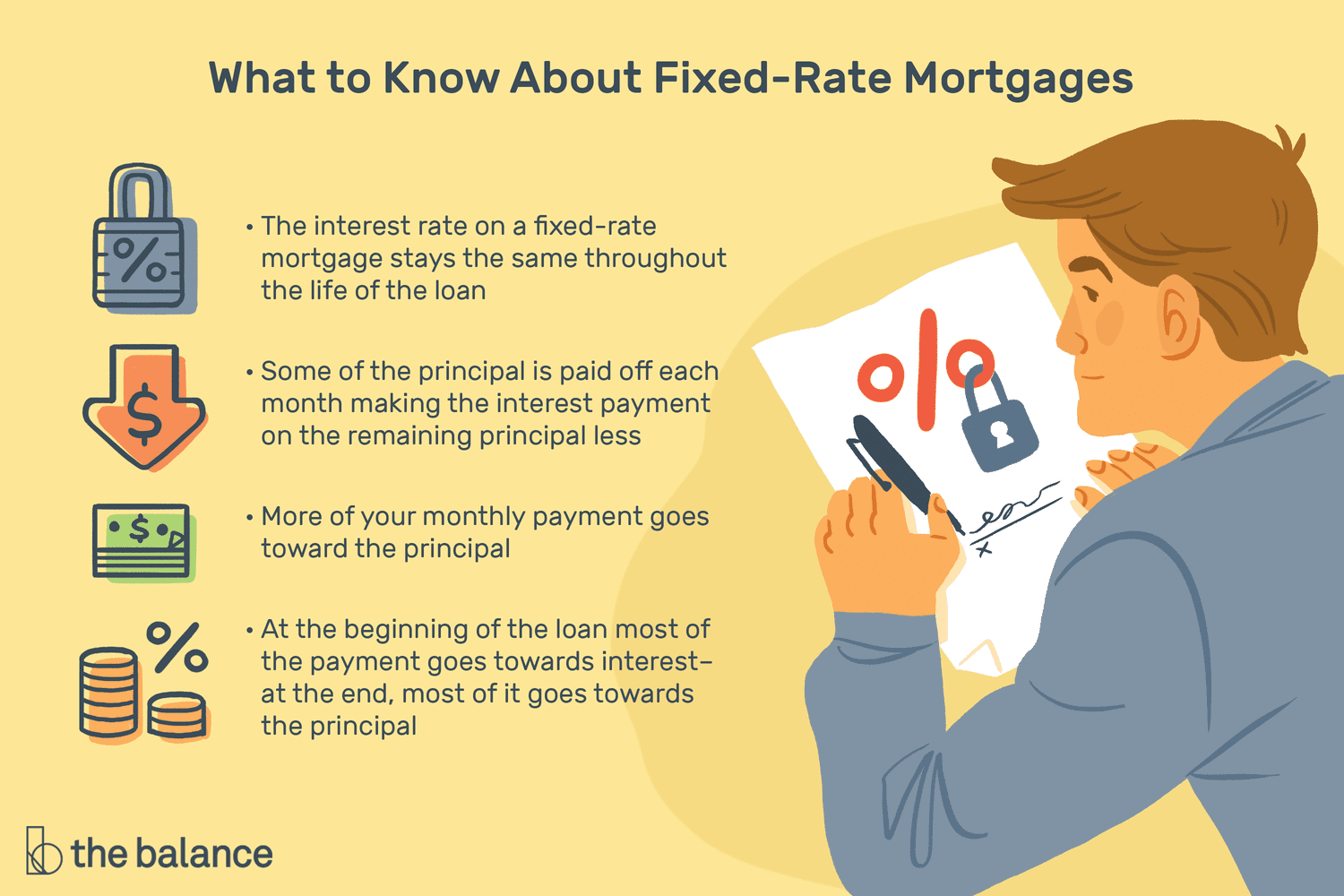

Key Takeaways

- What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage is a home loan where the interest rate remains the same throughout the life of the loan. This means your monthly payment stays consistent, making it easier to budget. - How It Works

Your monthly payment includes both interest and principal. Over time, more of your payment goes toward the principal, helping you build equity in your home. - Types of Fixed-Rate Mortgages

- 30-Year Mortgage: Lower monthly payments, ideal for long-term homeowners.

- 15-Year Mortgage: Higher monthly payments but faster equity buildup.

- 5/1 ARM: Fixed rate for the first five years, then adjusts annually.

- Pros and Cons

Pros: Predictable payments, protection from rising interest rates.

Cons: Higher initial rates compared to adjustable-rate mortgages, slower principal repayment. - How to Get One

Compare rates from banks, credit unions, and mortgage lenders. Use tools like the Consumer Financial Protection Bureau’s rate explorer to find the best deal.

What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage is a home loan where the interest rate remains constant for the entire loan term. This means your monthly payment stays the same, providing financial stability and predictability. Fixed-rate mortgages are available through banks, credit unions, and government-backed programs like FHA and VA loans.

Note: Your monthly payment may also include property taxes, home insurance, and mortgage insurance. These costs can increase over time, but your principal and interest payments will remain unchanged.

How Does a Fixed-Rate Mortgage Work?

Each monthly payment is divided into two parts:

- Interest: The cost of borrowing money.

- Principal: The amount you borrowed.

At the start of the loan, most of your payment goes toward interest. Over time, as you pay down the principal, more of your payment goes toward reducing the loan balance. This process is called amortization.

Example: If you have a $300,000 mortgage at a 4% interest rate, your initial payments will primarily cover interest. By the end of the loan, most of your payment will go toward the principal.

Types of Fixed-Rate Mortgages

- 30-Year Mortgage

- Pros: Lower monthly payments, ideal for long-term homeowners.

- Cons: Slower equity buildup, higher total interest paid over the life of the loan.

- 15-Year Mortgage

- Pros: Faster equity buildup, lower total interest paid.

- Cons: Higher monthly payments, greater risk of default if income drops.

- 5/1 Adjustable-Rate Mortgage (ARM)

- Pros: Lower initial interest rate.

- Cons: Rate adjusts after five years, potentially leading to higher payments.

Pros and Cons of Fixed-Rate Mortgages

Pros

- Predictable Payments: Your monthly payment stays the same, making budgeting easier.

- Protection from Rising Rates: Your interest rate is locked in, so you’re shielded from future rate hikes.

- Equity Buildup: You pay down the principal with each payment, increasing your home equity.

Cons

- Higher Initial Rates: Fixed-rate mortgages often have higher rates than adjustable-rate loans.

- Slower Principal Repayment: Early payments are mostly interest, so it takes longer to build equity.

- Higher Closing Costs: Fixed-rate loans may have higher upfront costs compared to ARMs.

How to Get a Fixed-Rate Mortgage

- Shop Around: Compare rates from multiple lenders, including banks, credit unions, and online lenders.

- Check Your Credit Score: A higher score can qualify you for lower interest rates.

- Calculate Your Budget: Use a mortgage calculator to determine what you can afford.

- Get Pre-Approved: Pre-approval shows sellers you’re a serious buyer.

- Understand the Terms: Look for a qualified mortgage that avoids risky features like balloon payments or negative amortization.

Alternatives to Fixed-Rate Mortgages

If a fixed-rate mortgage isn’t right for you, consider these options:

- Adjustable-Rate Mortgages (ARMs): Lower initial rates, but payments can increase over time.

- Interest-Only Loans: Pay only the interest for a set period, then start paying principal.

- No-Cost Loans: Closing costs are rolled into the loan, but you’ll pay more interest over time.

Frequently Asked Questions (FAQs)

1. What’s the difference between a 15-year and 30-year mortgage?

A 15-year mortgage has higher monthly payments but builds equity faster and costs less in interest. A 30-year mortgage has lower payments but takes longer to pay off and costs more in interest.

2. Can I refinance a fixed-rate mortgage?

Yes, refinancing can help you secure a lower interest rate or change your loan term.

3. What is a 5/1 ARM?

A 5/1 ARM has a fixed rate for the first five years, then adjusts annually based on market rates.

The Bottom Line

A fixed-rate mortgage offers stability and predictability, making it a great choice for long-term homeowners. However, it’s important to weigh the pros and cons and compare options to find the best fit for your financial situation. Use tools like the Consumer Financial Protection Bureau’s rate explorer to make an informed decision.

Want More Financial Tips?

Sign up for our newsletter to receive daily insights, analysis, and advice delivered straight to your inbox every morning!

This version is optimized for AdSense by:

- Using clear, engaging language to attract clicks.

- Structuring the content with headings, bullet points, and FAQs for readability.

- Highlighting key benefits and actionable advice.

- Emphasizing the importance of fixed-rate mortgages in financial planning and homeownership.